Veteran life insurance, explained

A plain-English guide to life insurance for veterans and their families, whether you are still serving, just left, or separated years ago.

Life insurance has one job. It replaces your income and pays off debts if you pass away. That money keeps a roof over your family and food on the table. For veterans, coverage comes from two places: the VA programs you earned through service, and private life insurance you buy on your own. This guide walks through both in plain terms, so you can see your life insurance options and pick what fits.

What veterans need to know first

While you serve, Servicemembers' Group Life Insurance (SGLI) covers you automatically. It is low-cost, easy to keep, and covers almost everyone. After you leave, your options open up. The right one depends on your health, your budget, and your family.

You have a few main paths. You can keep coverage through Veterans' Group Life Insurance (VGLI). You can buy a private term life insurance policy. Or you can use a VA program like VALife if you have a service-connected disability rating. If you are leaving soon, SGLI ends on a deadline, so line up new coverage before it does. And if you already own a policy, it is worth a second look.

Not affiliated with or endorsed by the U.S. Department of Veterans Affairs or any government agency.

The VA life insurance programs in brief

The VA runs several life insurance programs for the military community. Here are the three that matter most for veterans, plus family coverage.

SGLI (Servicemembers' Group Life Insurance)

SGLI is low-cost term life insurance for active-duty service members. It covers you for up to $500,000. Coverage ends 120 days after you separate from service. Read the full SGLI guide.

VGLI (Veterans' Group Life Insurance)

Veterans Group Life Insurance lets you keep your SGLI coverage amount after you leave, up to $500,000. Apply within 240 days of leaving and you skip the health questions. That makes VGLI a strong choice if your health is poor. The trade-off is cost. VGLI premiums rise as you age, and the jumps get steep later in life. Read the full VGLI guide.

VALife (Veterans Affairs Life Insurance)

VALife is guaranteed acceptance whole life insurance for veterans with a service-connected disability rating, even a 0% rating. Coverage caps at $40,000. Full benefits start two years after you apply, and you pay premiums during that wait. Veterans age 80 and under qualify, with no time limit to apply. Read the full VALife guide.

Coverage for your family

Family Servicemembers' Group Life Insurance (FSGLI) covers a service member's spouse for up to $100,000, and each child for $10,000 at no cost. Once you leave service, family SGLI ends too, so many families buy private coverage of their own. See life insurance for military families for spouse and child options.

Not affiliated with or endorsed by the U.S. Department of Veterans Affairs or any government agency.

Beyond the VA programs: your private options

Private life insurance is not one product. It comes in a few main types, and the difference is mostly about cost and whether the policy builds cash value.

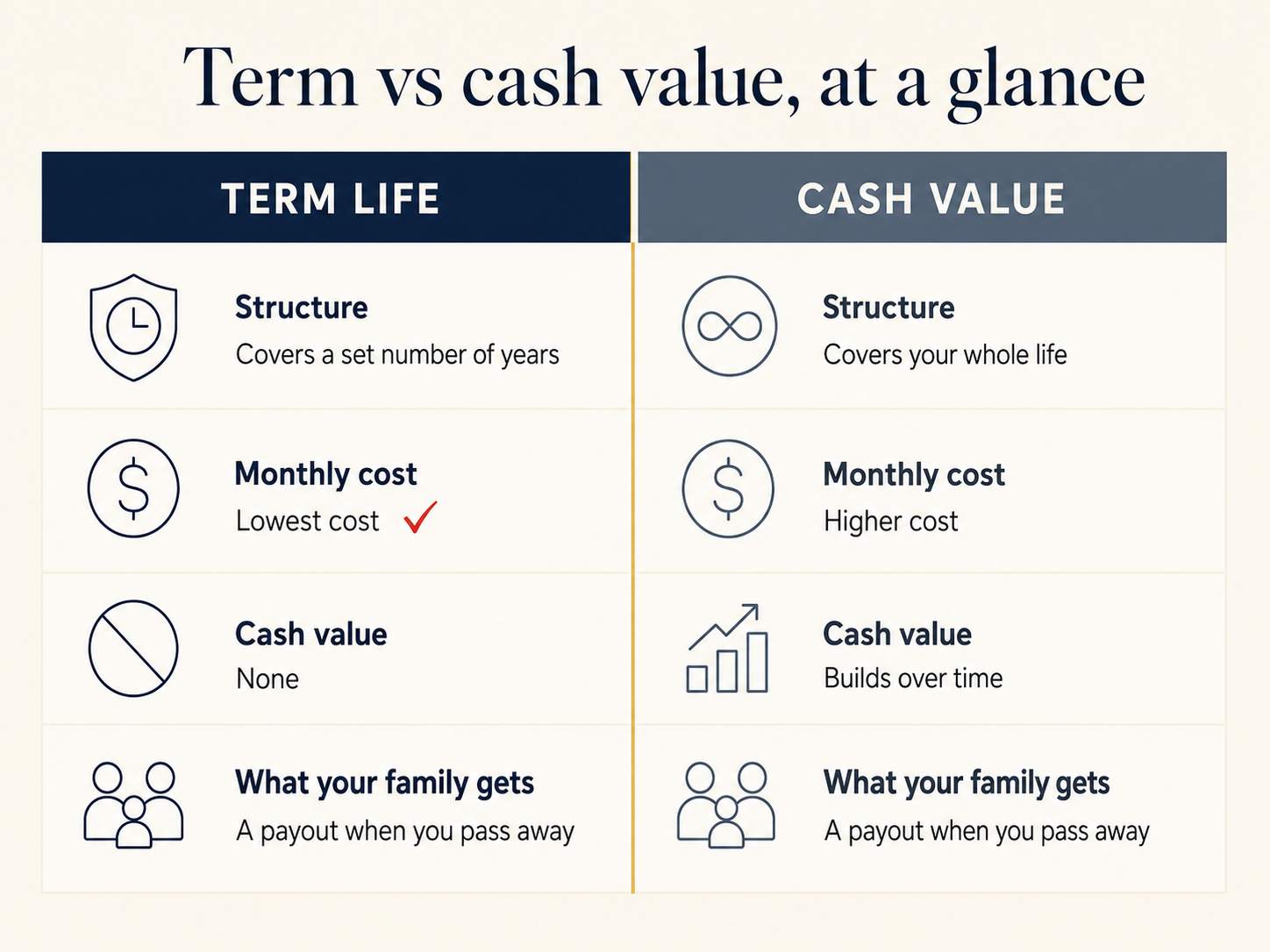

- - Term life insurance covers you for a set number of years at a level price. It is the simplest and lowest-cost type.

- - Whole life insurance is permanent life insurance. It lasts your whole life and builds cash value, at a much higher price.

- - Universal life insurance is permanent coverage with flexible payments.

- - Indexed universal life insurance (IUL) is permanent coverage tied to a market index, with caps and fees.

We teach all of these so you can compare them fairly. See them side by side on the types of life insurance page. Whole life, universal life, and IUL each cost more than term for the same coverage amount, because part of your payment funds the cash value.

Term keeps it simple and low-cost. Cash value policies cost more for the same coverage.

Private term life insurance

For many healthy veterans, a private term life policy is often the best fit. It locks in a level premium for 10, 20, or 30 years. Unlike VGLI, the price does not climb as you age. You pick the coverage amount and the length, and the cost stays flat for the whole term.

To get private term, you answer health questions or take a short medical exam. If you have serious health problems, VGLI may be your better route, since it skips the health review inside the 240-day window. That is why it pays to compare your choices before your VGLI window closes. See VGLI vs term life for the full comparison.

One more reason to act early: life insurance is priced on your health the day you apply. A level term policy locks that price in. Always answer health questions truthfully, and never delay medical care to qualify.

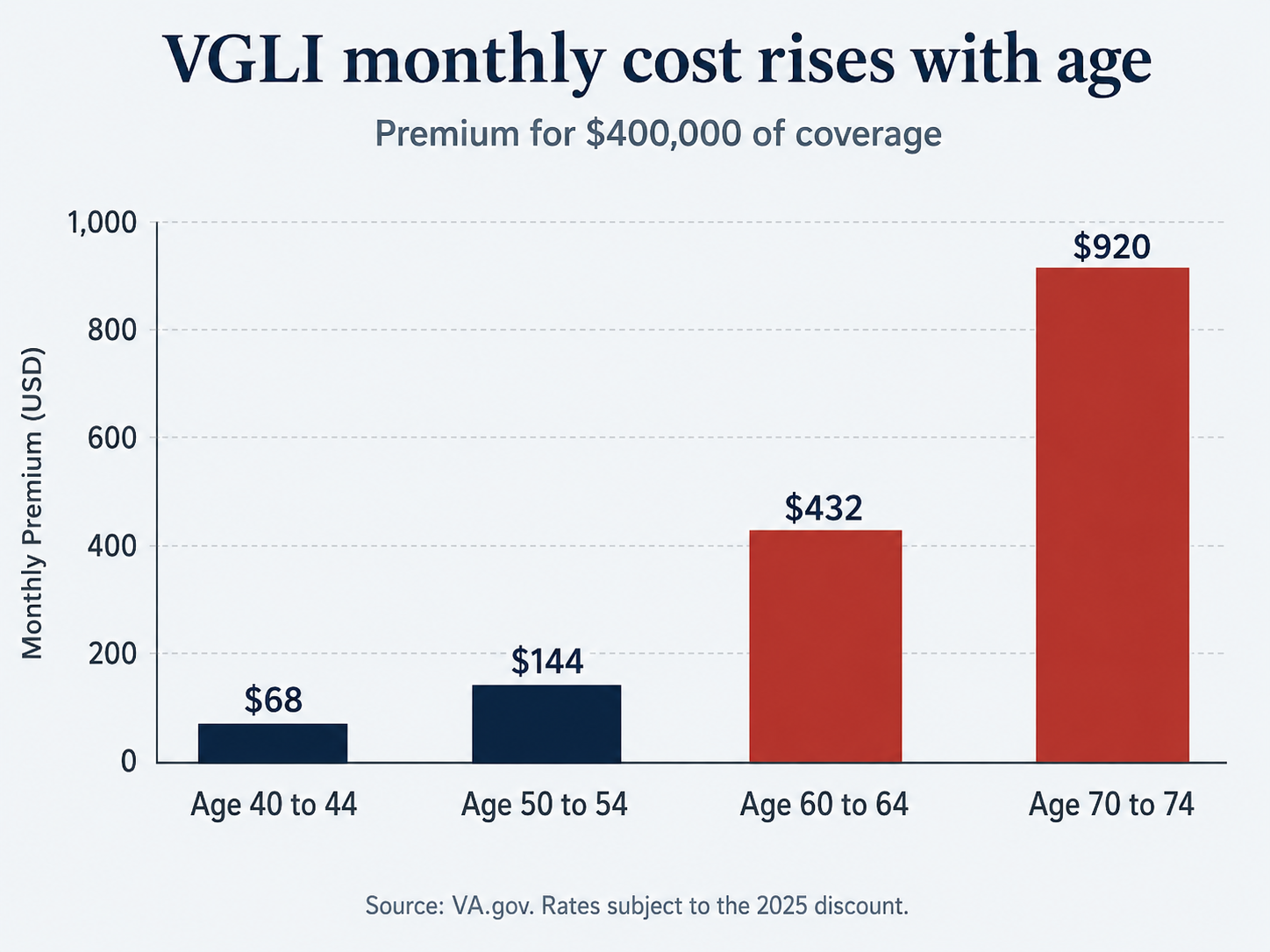

What VGLI really costs over time

VGLI is easy to keep, but the price is the trade-off. Premiums rise in five-year age bands, and the later jumps are large. Here is the pattern using VA's published rate chart for $400,000 of VGLI coverage.

| Your age | VGLI monthly premium ($400,000) |

|---|---|

| 40 to 44 | $68 |

| 50 to 54 | $144 |

| 60 to 64 | $432 |

| 70 to 74 | $920 |

Source: VA.gov VGLI premium rate chart. The VA applied a VGLI premium discount in 2025, so current rates may be lower. Check VA.gov for the latest figures.

VGLI cost rises with age. Source: VA.gov, rates subject to the 2025 discount.

The point holds. A level term policy bought while you are young and healthy can keep one price while VGLI keeps climbing. For a healthy veteran, that gap adds up to real money over 20 or 30 years.

How much coverage should you carry?

A common rule of thumb is 10 times your yearly income. The right number depends on your mortgage, your debts, and how much your family needs to keep their standard of living. Add up what you owe, what you want to replace, and future costs like college. Then size your life insurance coverage to match. Learn how much life insurance you need to size it for your situation.

VA programs vs private coverage

Both have a place. VA programs like VGLI and VALife accept you regardless of most health issues, which protects veterans who cannot pass a medical review. Private term life insurance usually costs less for a healthy veteran and locks the price for the full term. Many veterans use a mix. They keep a VA program if their health is a concern, and add private term while they are healthy enough to qualify.

The honest takeaway for most healthy veterans: level term gives you the most coverage for the lowest cost, and the price does not change as you age. If a health history makes private coverage hard to get, the VA programs are there. A licensed life insurance agent can review your situation and show you the numbers, at no cost.

Frequently Asked Questions

What to do next

You do not have to sort this out alone. Start with the free guide below. It lays out all your life insurance options as a veteran, the VA programs and the private ones, in plain language. When you are ready, a licensed life insurance agent can give you a free, no-pressure quote and review, on your schedule.

Get the free guide: The Veteran's Life Insurance Decision Guide.

Not affiliated with or endorsed by the U.S. Department of Veterans Affairs or any government agency.

The Veteran's Life Insurance Decision Guide

Get the free guide to all your life insurance options as a veteran, the VA programs and the private ones.